Featured

Table of Contents

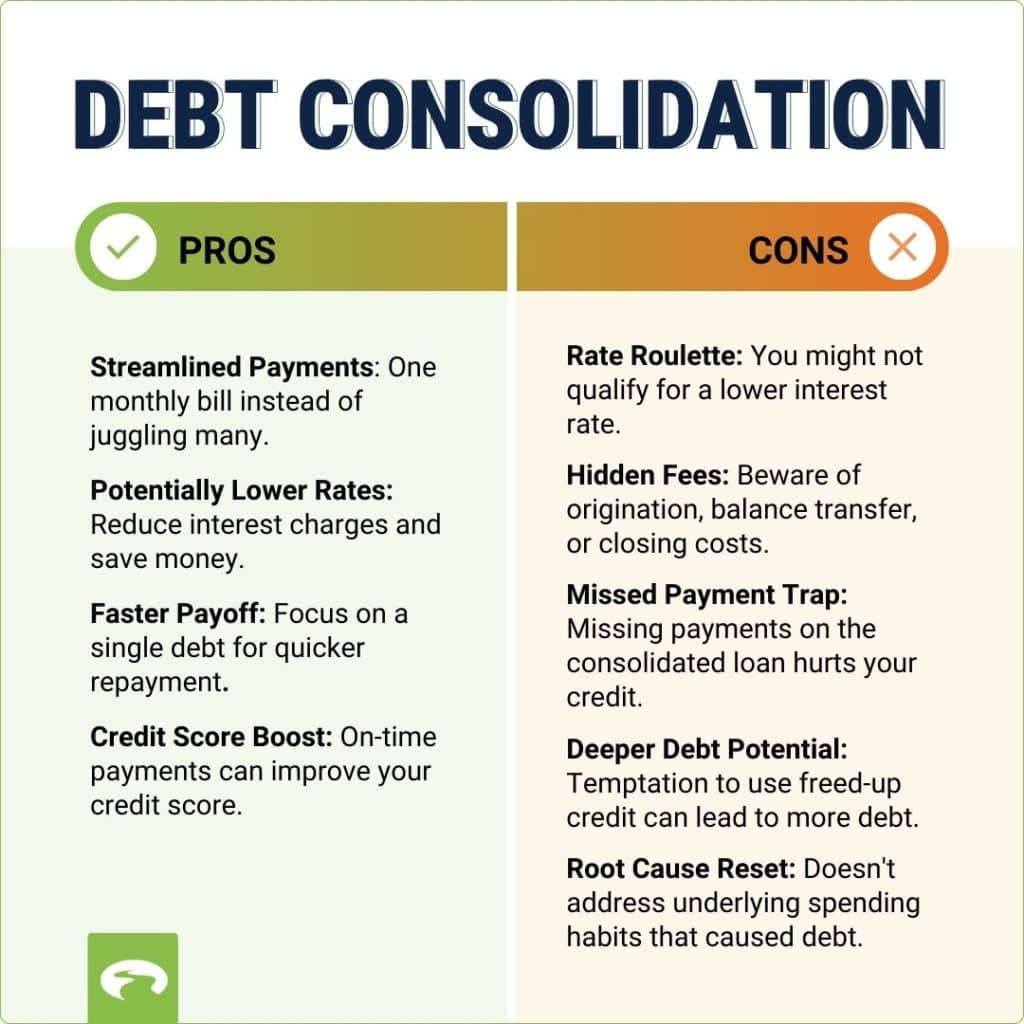

Financial obligation combination with an individual loan uses a few benefits: Repaired rate of interest and payment. Pay on multiple accounts with one payment. Repay your balance in a set quantity of time. Personal loan financial obligation combination loan rates are usually lower than charge card rates. Lower credit card balances can increase your credit report rapidly.

Consumers typically get too comfortable just making the minimum payments on their credit cards, however this does little to pay down the balance. In truth, making only the minimum payment can trigger your credit card debt to hang around for years, even if you stop using the card. If you owe $10,000 on a credit card, pay the typical charge card rate of 17%, and make a minimum payment of $200, it would take 88 months to pay it off.

Contrast that with a debt consolidation loan. With a financial obligation combination loan rate of 10% and a five-year term, your payment only increases by $12, but you'll be without your financial obligation in 60 months and pay simply $2,748 in interest. You can use a personal loan calculator to see what payments and interest may look like for your financial obligation consolidation loan.

The rate you receive on your personal loan depends on many aspects, including your credit rating and earnings. The smartest method to know if you're getting the very best loan rate is to compare offers from completing loan providers. The rate you get on your debt combination loan depends on many factors, including your credit history and income.

Financial obligation combination with an individual loan may be best for you if you satisfy these requirements: You are disciplined enough to stop carrying balances on your credit cards. Your personal loan rate of interest will be lower than your credit card interest rate. You can pay for the individual loan payment. If all of those things do not use to you, you might require to look for alternative ways to consolidate your debt.

Essential 2026 Planning Calculators for Borrowers

Sometimes, it can make a financial obligation issue even worse. Before consolidating debt with an individual loan, consider if among the following scenarios uses to you. You understand yourself. If you are not 100% sure of your capability to leave your credit cards alone once you pay them off, do not combine debt with an individual loan.

Personal loan interest rates average about 7% lower than credit cards for the same borrower. If you have credit cards with low or even 0% introductory interest rates, it would be ridiculous to change them with a more costly loan.

In that case, you might desire to use a charge card debt consolidation loan to pay it off before the penalty rate kicks in. If you are simply squeaking by making the minimum payment on a fistful of credit cards, you may not have the ability to lower your payment with a personal loan.

The Comprehensive Review of Modern Credit ReliefAn individual loan is developed to be paid off after a particular number of months. For those who can't benefit from a debt consolidation loan, there are options.

Comparing Debt Management versus Loans in 2026

If you can clear your financial obligation in less than 18 months or so, a balance transfer credit card might provide a quicker and less expensive alternative to a personal loan. Customers with outstanding credit can get up to 18 months interest-free. The transfer charge is generally about 3%. Make certain that you clear your balance in time, however.

If a debt consolidation payment is too high, one way to decrease it is to extend out the payment term. One method to do that is through a home equity loan. This fixed-rate loan can have a 15- or perhaps 20-year term and the rate of interest is extremely low. That's since the loan is secured by your home.

Here's a comparison: A $5,000 personal loan for financial obligation combination with a five-year term and a 10% interest rate has a $106 payment. Here's the catch: The overall interest cost of the five-year loan is $1,374.

New Methods for Reaching Financial Freedom

If you truly require to decrease your payments, a second home loan is a great option. A debt management strategy, or DMP, is a program under which you make a single regular monthly payment to a credit therapist or debt management professional.

When you enter into a strategy, understand just how much of what you pay each month will go to your financial institutions and just how much will go to the business. Learn how long it will take to end up being debt-free and make sure you can manage the payment. Chapter 13 bankruptcy is a financial obligation management plan.

One advantage is that with Chapter 13, your lenders need to get involved. They can't pull out the way they can with debt management or settlement strategies. Once you submit insolvency, the bankruptcy trustee identifies what you can realistically afford and sets your monthly payment. The trustee disperses your payment amongst your lenders.

Released amounts are not gross income. Financial obligation settlement, if effective, can discharge your account balances, collections, and other unsecured debt for less than you owe. You normally provide a lump amount and ask the financial institution to accept it as payment-in-full and compose off the remaining unsettled balance. If you are very a great mediator, you can pay about 50 cents on the dollar and bring out the financial obligation reported "paid as concurred" on your credit rating.

Using Debt Estimation Tools for 2026

That is extremely bad for your credit rating and rating. Any amounts forgiven by your financial institutions are subject to earnings taxes. Chapter 7 insolvency is the legal, public variation of debt settlement. Just like a Chapter 13 bankruptcy, your lenders must participate. Chapter 7 insolvency is for those who can't afford to make any payment to reduce what they owe.

The downside of Chapter 7 personal bankruptcy is that your possessions need to be offered to satisfy your financial institutions. Debt settlement enables you to keep all of your belongings. You just provide cash to your lenders, and if they accept take it, your belongings are safe. With personal bankruptcy, discharged financial obligation is not taxable income.

Follow these pointers to guarantee an effective debt payment: Find a personal loan with a lower interest rate than you're presently paying. In some cases, to pay back debt quickly, your payment needs to increase.

{kind=link}

Latest Posts

Smart Methods for Reducing Consumer Debt in 2026

Leveraging Financial Estimation Tools for 2026

Reducing High APR for 2026 Loans